Photo by PhotoPum RanaRoja on Unsplash

Kishen Mangat VP/GM Cisco Mobility Group - June 20, 2018

As we head into the summer of 2018 and as the heat starts to roll in, the world’s mobile operators find their networks in a similar position – HOT! With all of the new mobile & IoT devices soon receiving gigabit access anywhere where 5G and LTE-A are available, the consumer and business person will soon experience a full-scale ability to unshackle from their physical office and become road warriors.

What’s driving the uptick in the mobile traffic?

Mobile Video, IoT, Enhanced Mobile Broadband

With the recent announcements of “merger mania” in the video and mobile market, we expect the mobile video growth to continue to skyrocket, putting additional strain on the mobile infrastructure. As the old saying goes, “if you can’t beat them, join them.” Well, many service providers are doing just that to compete against the video Over-The-Top (OTT) providers, with reactions such as AT&T’s acquisition of DirecTV (and recently approved acquisition of Time Warner),, Verizon’s completion of its purchase of AOL & Yahoo, Vodafone’s acquisition of ONO, as well as many other service providers looking to acquire additional video assets.

According to Machina Research, the number- of Internet of Things (IoT) connected devices are predicted to grow to 27 billion devices by 2025. That number includes sensors to mission critical applications. All those devices—connected—by 2025. It’s pretty easily to see the challenge that mobile network operators will have to contend with (and plan for).

According to Statista.com in 2011, there were almost 1.2 billion mobile broadband subscriptions worldwide. The number of unique mobile subscribers worldwide is forecasted to increase from around 4.82 billion in 2016 to 5.69 billion by 2020. With the vast adoption of mobile phones worldwide, the mobile industry has not only changed in scale, but also in use.

The need to differentiate

The mobile service provider will not differentiate themselves by the 5G radio or first mover advantage alone, as every mobile operator on the planet has either some sort of 5G proof-of-concept in place or a vision to get there at some point. The mobile service provider will need to differentiate themselves by delivering new cloud services and enhanced connected experiences to consumers and businesses. The mobile service provider will need a multi-cloud-to-client, multi-vendor network that is highly automated, able to partition network resources through network slicing, and able to quickly deliver services where and when they are needed. These operators will need to provide visibility and security for their business customers and for themselves.

Additionally, the mobile service provider will need to think differently about how they bundle and tariff their services. Today, as has been done since Watson was charged 5 cents for his call with Mr. Bell, service providers typically charge by session (call) and by bandwidth offered. This costing structure is easy to compete against and offers nothing to foster loyalty from the customer. Smart bundles that reflect how these connected services are experienced will provide a more unique relationship. For example, recently a tier-1 provider in Asia announced IoT service for 10 cents per device per month (maximum 10K bandwidth consumed). Perhaps a better pricing model would be to focus on the manner of usage or experience. For example, an offering for the consumer might include something like a whole smart home package for $20 per month (up to 15 devices) and a secured smart home package for $30 per month (using Cisco Security solutions). This sort of bundle is geared to the outcome and experience and can offer a level of service that build loyalty.

Industry leading Ultra Packet Core

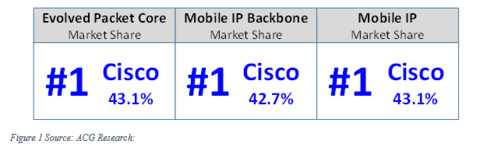

Cisco’s Ultra Packet Core (UPC) is the industry-leading, cloud-native converged mobile core. As evidenced by recent quarterly announcements by ACG Research, and by IHS Markit (formally Infonetics Research), Cisco is and has been the true leader in the Evolved Packet Core (EPC) market for several consecutive quarters. For example, Cisco has held the #1 position for EPC market share in ACG Research’s results for over four years.

- Converged next-gen mobile core supports 5G, 4G, 3G, Wi-Fi, Small Cells, and IoT

- Distributed edge services and intelligence

- Network slicing across both 5G and 4G

- Enhancements to support massive scale IoT (and 5G)

- Two new optimization licenses (Traffic and TCP)

- Ability to supply premium revenue generating customer service experiences

- And much more…

Market Share Leader in Worldwide Evolved Packet Core (MME, PGW & SGW) & Mobile IP Backbone & Mobile IP Infrastructure

Summation

The Cisco Ultra Packet Core is leveraged today by more than 80 mobile operators across the globe and growing rapidly, with more than 40 of those operators in commercial operation with the cloud-based platform. Today, our UPC is carrying more than 300 million users and continuing to flourish, soon the platform will have more than 600 million users traversing in the next few months.

Our bespoke ASR5500 platform is still growing at a healthy growth rate as well where we are deployed in more than 350 mobile operator networks, carrying well over 1 billion users today on that platform. So as the operators decide the time is right to transition to cloud based solution it is a simple transition for the operator as the features are the same.

For the full ACG Research report, please go to http://acgcc.com

For more information see our Cisco’s LTE Solutions.

For more on Cisco 5G Strategies and Solutions.

For more information on IHS Markit please go to https://technology.ihs.com/AboutUs

For more details on Machina Research: https://machinaresearch.com

Meanwhile, we’d love to hear from you on what you’re looking forward to in the mobile market. Tweet us @CiscoSPMobility for questions or comments.