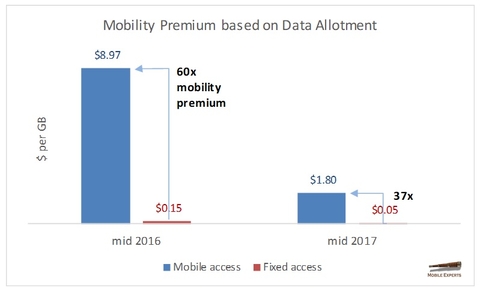

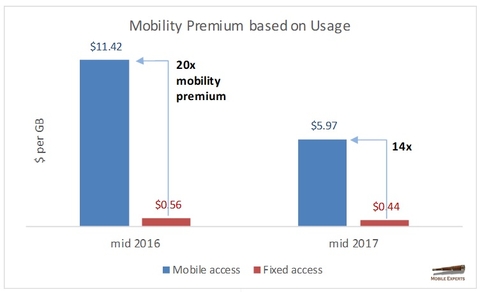

Last year, we wrote about mobility premium, an index to compare the pricing difference on a dollar-per-gigabyte basis between fixed and mobile broadband services. A little over a year ago, the mobility premium in the U.S. stood at 20x to 60x based on actual usage or based on data allotments of popular family share plans, and we predicted that the mobility premium will trend downward as a possible competition between fixed and mobile operators rises.

A lot has happened since. The competition in the U.S. mobile industry has been unrelenting with “unlimited” plans now being the norm. After a series of promotions and unlimited data service plans, the weighted average mobile broadband pricing has come down fivefold from about $9 per GB in 2016 to $1.80 per GB this year. Meanwhile, the cable operators, who dominate the fixed broadband market, have upped monthly data caps on popular high-speed Internet plans from 300 GB to 1 TB. As a result, on a data allotment basis, the mobility premium has decreased from 60x to 37x in just one year.

The mobility premium based on usage is arguably a closer reflection of consumer value preference since it is based on actual usage and not on market pricing plans which implicitly reflect operators’ view of consumer demand.

The cable/mobile M&A rodeo is about to begin, and the “mobility premium” is an important factor for all players.

Kyung Mun is a senior analyst at Mobile Experts LLC. Mobile Experts is a network of market and technology experts that provides market analysis on the mobile infrastructure and mobile handset markets. Over the course of his 20+ years in wireless and cable industries in a dynamic range of roles from engineering to product management and technology strategy, Mun has contributed to the advancement of mobile communication while working at leading companies in the mobile value chain including Motorola, Texas Instruments, Alcatel-Lucent and a few startups in between. He holds undergraduate and graduate degrees in electrical engineering from the University of Texas at Austin and Georgia Tech, and studied finance and strategy at Southern Methodist University.